By Nick Green on October 27, 2020 at 5:27 PM

When news of the new Individual Coverage Health Reimbursement Arrangement (ICHRA) broke last year, most everyone in the healthcare industry, employee benefit advisors, tax professionals, and technology providers asked the same general question—how will employers adopt ICHRA?

As a new health benefit for 2020 with more flexibility than previous HRAs, interest began almost immediately. Suddenly, employers of all sizes could use a reimbursement model for their health benefit. Applicable Large Employers (ALEs) could use an ICHRA to satisfy the ACA’s employer mandate. Employees could be grouped into classes to determine benefit eligibility and allowance amounts. With these and other tools at their disposal, 800,000 organizations are expected to offer an ICHRA by 2024.

PeopleKeep was the first company to deliver an ICHRA product to market. We started taking orders in September 2019 for employers seeking the first available benefit effective date of January 1, 2020. Over the past nine months, we have been privileged to work with many early adopters of ICHRAs and learn along the way.

We have analyzed customer data from the first nine months of ICHRA availability and compiled it into the following report, which shows how ICHRA customers are using the new health benefit to offer health benefits for the first time or replace traditional offerings like group health insurance. We also made an infographic to highlight our key findings.

This report covers everything from which classes employers are using to average allowance amounts to the most common reimbursed expenses.

Table of Contents

I. Classes

i. State-based classes

II. Allowances

i. Allowances based on reimbursable expenses

ii. Allowances based on company size

III. Expenses

IV. Conclusion

Classes

One of the most compelling parts of the ICHRA is the ability to group employees into classes. The ICHRA final rules define 11 classes employers can use to determine employee eligibility and allowance amounts. Classes can also be combined and layered on top of each other to create custom classes.

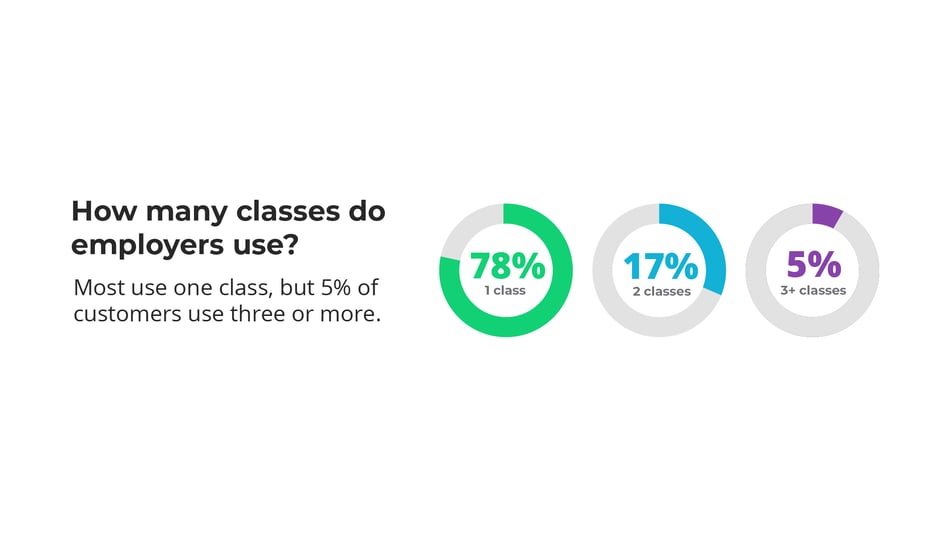

We found that most employers decided to keep the benefit simple when it comes to classes: 78% of employers used one class when designing their benefit. Only 5% of employers used more than two classes, while no employers used more than five.

The most common classes our customers are using, not including any that may also include a state-based criterion, in order of popularity are:

- All employees

- Full-time salaried employees

- Full-time employees

- Salaried employees

- Part-time employees

- Full-time hourly employees

- Seasonal employees

State-based classes

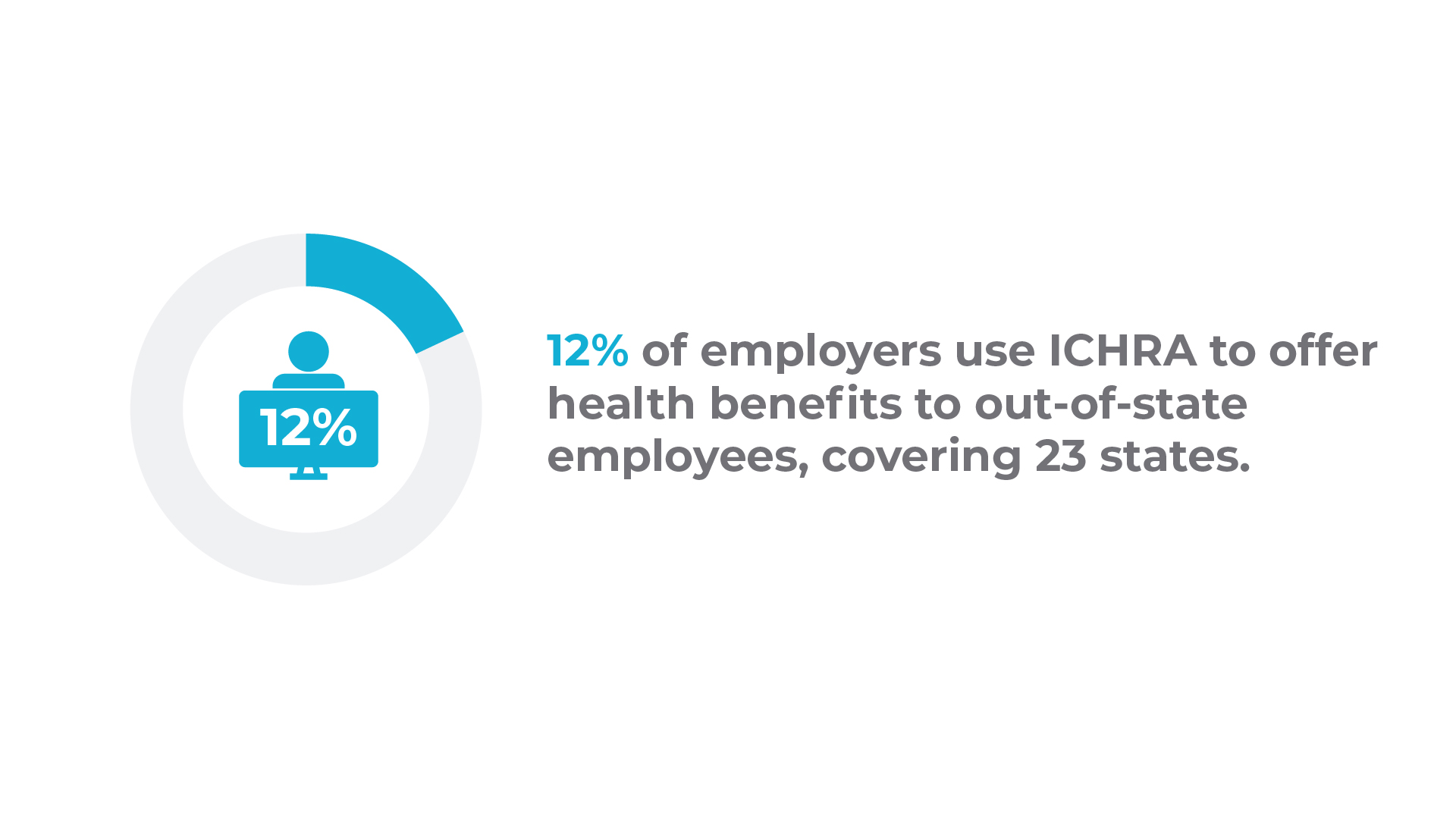

A popular use case for ICHRA has been employers who have employees across state lines. In fact, 12% of PeopleKeep ICHRA customers used a class that included state-based criteria.

Many of these employers already offer a group health insurance plan to their employees in the state where their organization is headquartered, but they still want to do something for their employees in other states who aren’t eligible for the group plan. ICHRA is a great fit in this case because it allows these employers to put their out-of-state employees into a class and offer them an ICHRA without making any changes to their current group plan.

For employers with widely distributed team members, ICHRA also works well. PeopleKeep customers have added classes for 23 states. The average number of state-based classes for employers using them is 1.73, ranging from one to seven.

Employers in 38 states have partnered with PeopleKeep to offer an ICHRA.

Allowances

Once an employer defines their classes, they’re still able to vary allowances within the class using family status.

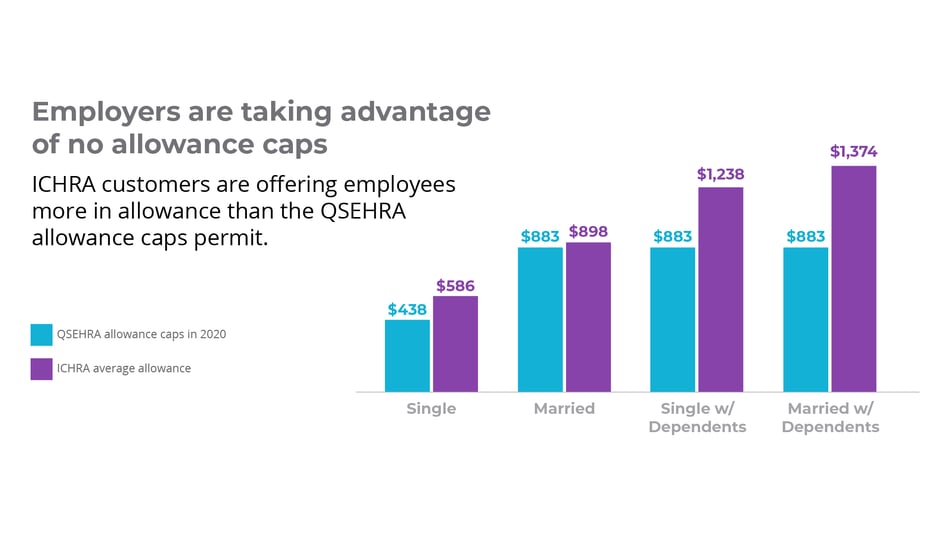

Unlike the Qualified Small Employer HRA (QSEHRA), the ICHRA doesn’t have allowance caps. That means an employer can offer as much as they want based on what they can afford.

Our report finds that employers offering an ICHRA tend to offer more than the QSEHRA allowance caps allow. In 2020, the monthly QSEHRA allowance caps are $437.50 for single employees and $883.33 for single employees with dependents, married employees, and married employees with dependents. In that order, our analysis shows the average monthly ICHRA allowance amounts for those statuses are $586.41, $898.23, $1,237.95, and $1,374.28.

So, for single employees, employers offering an ICHRA are providing, on average, a benefit that is 34% larger than the maximum amount allowed with a QSEHRA. That difference is even larger for married employees with dependents, who receive an ICHRA allowance that’s 56% larger, on average, than the maximum under a QSEHRA.

The overall average monthly allowance was $840.19, but we wanted to dig deeper to see if the allowances changed when different criteria were met. To that end, we broke down allowances based on allowable expenses and company size to give a more targeted look at how different organizations use the benefit.

Allowances based on reimbursable expenses

It turns out that there is a vast difference in the allowance amounts offered by employers who allow reimbursement of both insurance premiums and out-of-pocket expenses compared to those who only reimburse employees for premiums. It stands to reason that employers who are able and interested in broadening the type of expenses they reimburse would also want to make more money available to their employees for those expenses. What was unexpected was the degree to which that is true.

Those who reimburse both premiums and out-of-pocket expenses offer at least 80% more in monthly allowances to employees in each status. The greatest discrepancy is in the married status, where employers who reimburse both offered 93% more in monthly allowances.

Allowances based on company size

In general, larger companies have more revenue and therefore more money to set aside for health benefits. Following this thinking, it wouldn’t be a stretch to say that larger companies would offer their employees more in allowance. The reality, however, is the complete opposite.

PeopleKeep’s ICHRA customers offered less money in monthly allowances across all employee statuses as their employee count grew. The smallest cohort, 1 - 4 employees, offered at least 106% more in monthly allowances than the largest cohort, 50+ employees. The largest difference came in the single status where employers with 1 - 4 employees offered 234% more in monthly allowances than their 50+ employee counterparts.

While they may have less revenue, smaller employers tend to have a few key employees whom they really want to hire or keep around. Offering a generous allowance in these situations is doable. Expanding that generous allowance to all 50+ employees can quickly become unsustainable. ALEs may also have different motivations than their smaller counterparts. Since they’re mandated to offer a group health plan by the ACA, it’s possible they’re offering a health benefit mostly out of necessity and may be less concerned about offering as much as possible to all of their employees.

Expenses

One of the first choices an employer makes when setting up an ICHRA is whether to reimburse employees only for insurance premiums or to include out-of-pocket expenses as well. 63% of PeopleKeep ICHRA customers choose to reimburse their employees for both premiums and out-of-pocket expenses.

There are hundreds of possible eligible expenses that employees can be reimbursed for. If you’re curious, the full list can be found on IRS Publication 502. With so many options, we wanted to see which expenses get reimbursed the most. The five most common expenses employees have been reimbursed for in terms of percentage of users with non-premium expenses who submitted the expense are:

- Prescription drugs (69% of all users who submitted a non-premium expense)

- Medical office visits (49% of all users who submitted a non-premium expense)

- Dental care (27% of all users who submitted a non-premium expense)

- Chiropractic care (12% of all users who submitted a non-premium expense)

- Psychiatric therapy (5% of all users who submitted a non-premium expense)

Choosing to include these expenses makes the benefit even more valuable for employees, but only makes sense if you can afford to offer more in allowance than your employees pay in premiums. Otherwise, the allowance will be spent on premiums regardless of the other expenses you allow to be reimbursed.

Reimbursing employees for common expenses is valuable since employers will be helping to ease a burden their employees face on a regular basis. However, not all expenses are common. Reimbursing these uncommon, and sometimes expensive, expenses can be invaluable to employees.

The most costly expenses in terms of average amount per expense are:

- Wheelchair and repairs ($4,478.16 per expense)

- Hearing aids and batteries ($3,925 per expense)

Conclusion

The first nine months have taught us a lot about which employers are drawn to the ICHRA and how they use it to meet their health benefits goals. The ICHRA has proven to be a great fit for employers who want more control over their health benefits costs than a group health insurance plan can provide but want to offer more in allowances than the QSEHRA will allow. For employers with a distributed workforce, it’s also a very attractive approach.

If you’d like to learn more about the ICHRA and see if your organization could benefit from offering one, schedule a call with one of our Personalized Benefits Advisors.

ICHRA vs. employer health insurance stipend

Compare ICHRA vs. stipends and cash bonuses. Learn why a formal ICHRA lets you fund employee health plans 100% tax-free without payroll tax.

5 steps to a successful ICHRA launch

Discover 5 key steps to a successful ICHRA setup. Learn how to implement, communicate, and manage your ICHRA to offer flexible health benefits.

How does COBRA interact with ICHRA?

Learn how COBRA interacts with ICHRA. Discover the rules for continuing health coverage and how ICHRA reimbursements apply under COBRA.