By Christina Merhar on August 6, 2013 at 2:50 PM

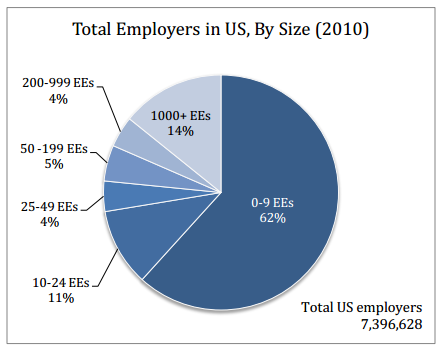

Small businesses make up the majority of employers in the US, and yet studies show that small businesses struggle the most with offering health insurance. There are approximately 7.4 million employers in the US, and the majority are micro and small businesses.

-

82% of all US employers (6 million employers) have less than 200 employees

-

62% of all US employers (4.6 million employers) have less than 10 employees

2.37 Million Small Businesses Don't Offer Health Insurance

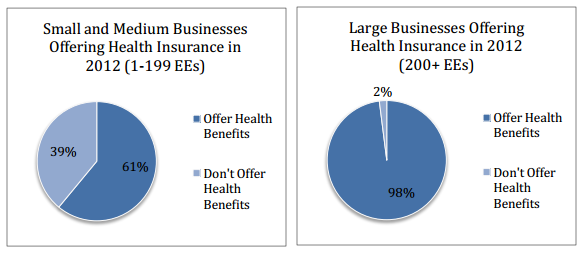

Small and medium sized businesses (82% of all US employers) struggle to offer health insurance to employees. Studies show that the smaller the business, the less likely they are to offer health insurance:

-

98% of all larger businesses (200+ employees) offer health insurance.

-

39% of all small and medium businesses (< 200 employees) do not offer health insurance.

-

50% of all micro employers (< 10 employees) do not offer health insurance.

That's 2.37 million small businesses that don't offer health insurance.

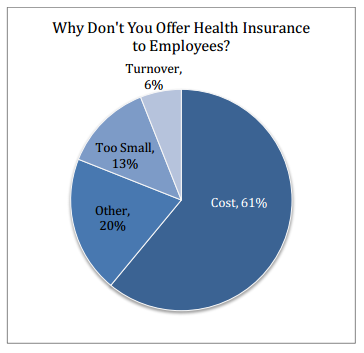

Primary Reason Small Businesses Don't Offer Health Insurance? Cost

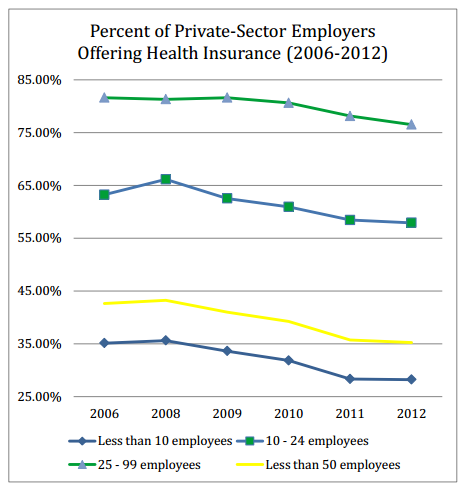

Premiums are rising so quickly that small business owners are often dealt annual renewal rates they cannot afford. Between 1999 and 2012, group health insurance premium rates to cover a single employee increased from $2,196/year to $5,615/year.

These cost increases have been reflected in the declining rates of small businesses offering health insurance, especially among employers with less than 10 employees.

Also, when small business owners are surveyed about the primary reason they do not offer health insurance, 61% say it's because of cost.

The Solution? Alternatives Such as Defined Contribution

Because of the increase in premium costs and because of new health care reform changes, experts predict that up to 60% of educated employers plan to pursue alternatives to offering health insurance by 2014, including “defined contribution”.

With a "pure" defined contribution approach, the small business offers healthcare allowances instead of a traditional group health insurance plan. The small business simply uses the defined contribution health plan to reimburse employees tax-free for their personal insurance policies.

A "pure" defined contribution health plan allows the small business to completely define and control the cost of employee health benefits, while providing employees' access to the same or better health insurance coverage.

Do small businesses have to offer health insurance?

Wondering about small businesses and health insurance obligations? This guide explains whether small businesses are required to offer health coverage.

How to make individual health insurance work for small employers

Wondering how small businesses can use individual health insurance? Discover strategies to offer flexible, affordable coverage to your employees.

2 Minute Guide to Small Business Health Insurance Options

Small Business Health Insurance Options. A look at health insurance options for small businesses in 2014 and beyond.