By Elizabeth Walker on June 15, 2026 at 10:00 AM

For many employers, health insurance isn’t a typical employee benefit. It’s the most important and most expensive benefit you can offer. Driven by rising hospital costs, increasingly chronic health conditions, and growing demand for specialty medications, employer healthcare costs have been steadily increasing over the past decade. As a result, business owners are asking an important question: How much does health insurance actually cost per employee?

If you want to forgo offering a health benefit to save money, that could be a mistake. Employees consistently rank health coverage as their most valued benefit, with a PeopleKeep survey finding that 92% of employees value it. Organizations that don't offer it may struggle with employee retention.

Understanding what employers typically pay for health insurance and the alternative options available can help you build an employee benefits package that supports your budget.

In this blog post, you’ll learn:

- How much employers and employees typically pay for group health insurance premiums, and the factors that influence those costs.

- What drives rising healthcare expenses, and how employers can control their budgets.

- How alternatives like health reimbursement arrangements (HRAs) can help employers offer flexible and affordable health benefits.

How much does group health insurance cost?

There are two primary types of group health insurance: fully-insured and self-funded. When an employer provides fully-insured traditional health coverage to employees, they purchase a plan (or plans) from an insurance carrier or broker to cover all eligible employees and, in some cases, their spouses and dependents.

While group health plans are familiar to most employees, they have minimum participation requirements, a “one-size-fits-all” structure that may not support every employee’s needs, and have high costs.

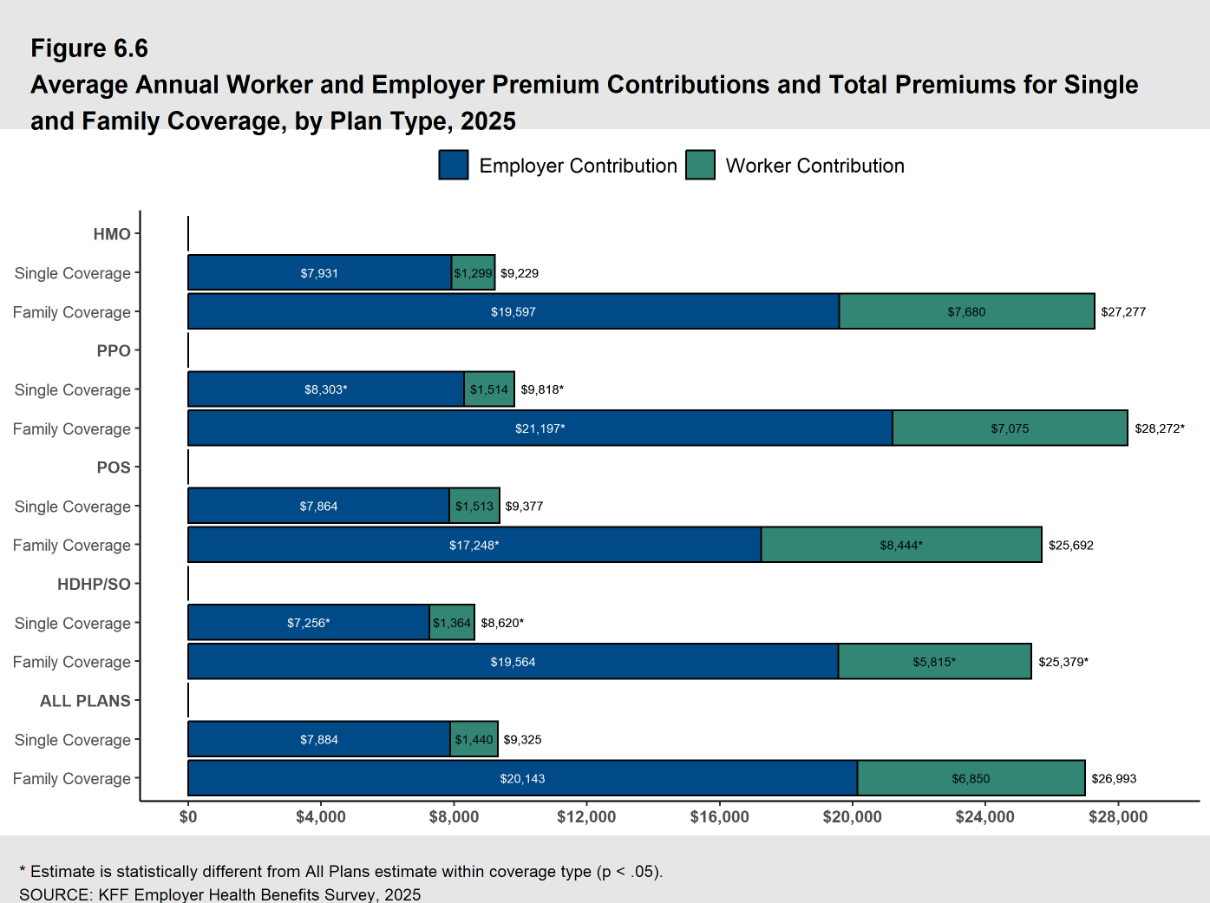

According to KFF’s Employer Health Benefits Survey, in 2025, the average annual cost of employer-sponsored health insurance premiums per employee was $26,993 for family coverage and $9,325 for single coverage1. Although specific costs will vary due to many key factors, like your health insurance company and company size, the average cost of group health plans typically increases annually.

Self-funded plans are also group health plans, but the employer directly covers employee medical expenses. While employers don’t pay premiums for self-funded coverage (though they can pay for stop-loss policies), they’re responsible for the actual medical claims and the risk that comes with it. They can pay a third-party administrator or insurance carrier to administer the benefit.

In addition to traditional health insurance, many employers also offer telemedicine options and provide wellness program incentives to encourage their employees to identify health issues early on and manage chronic conditions.

How much do employers pay for health insurance?

If you’re an employer offering health benefits for the first time, ensuring you have the budget to help your employees with the cost of the health benefit is fundamental to retaining talent and attracting new employees. The portion you pay toward the cost of employees’ health coverage will vary based on your company, but we’ll give you an idea of the average contribution amounts.

In 2025, the average amount of money employers contributed toward group health insurance premium costs was 75% for family coverage and 85% for single plans. This equated to $20,143 annually for family policies and $7,884 annually for single coverage per employee. The average of family premiums has increased 26% over the last five years and 47% during the previous ten years.

Image: KFF

How much does group health insurance cost for employees?

Looking again at KFF’s Survey, in 2025, group health insurance plans cost employees $6,850 annually for family coverage and $1,440 annually for single coverage. They contributed 25% and 15%, respectively, toward the total cost of family and single coverage premiums. Employees typically pay their monthly premiums through payroll deductions on a pre-tax basis.

Premiums tend to rise every year. PwC’s Health Research Institute reported that average healthcare increases remain at 8.5% for group insurance plans and 7.5% for the individual market. While this has been the same projected rate for the past three years, it’s a 3% increase since 2022.2

How you can control group health insurance costs

Healthcare is one of the most expensive benefits you can offer at your organization. However, it’s one of the most valued benefits employees can receive. By better understanding what factors affect your health benefits costs, you can gain greater control over your budget and set your employees up for success.

Typical factors that will affect the cost of employer-sponsored health plans include:

- Your enrolled employees’ ages and family sizes

- For example, older workforces may have health conditions that result in higher medical costs, which might increase your rates.

- The number of employees participating in the group plan

- Your location

- The health plan type, such as a preferred provider organization (PPO), point of service (POS), exclusive provider organization (EPO), or health maintenance organization (HMO)

- Plan features, such as annual deductibles, copayments, and the out-of-pocket maximum

- Your company’s medical claim history

- Industry

- Any add-on benefits to the plan, such as ancillary benefits

Keep in mind that how insurers determine the cost of group plan premiums varies depending on whether your employer has a large or small group health plan. For example, insurers can only vary premiums for small group plans by age, family size, location, tobacco use, and plan type.

How you can use an HRA to provide your employees with affordable healthcare coverage

If covering the cost of a group plan and paying its associated health premiums is out of reach for your organization, you can opt for a health reimbursement arrangement (HRA). With an HRA, you can reimburse your employees, tax-free, for their qualified medical expenses. Depending on the type of HRA, individual health insurance premiums may also be eligible for reimbursement.

The qualified small employer HRA (QSEHRA) and the individual coverage HRA (ICHRA) are two stand-alone HRAs that work well for employers looking for flexibility and cost predictability. Better yet, they can replace group health insurance plans.

The 21st Century Cures Act created the QSEHRA specifically for small businesses with fewer than 50 full-time equivalent employees (FTEs). ICHRAs are similar to QSEHRAs, but they’re for employers of any size and have more customization options.

You can also offer a group coverage HRA (GCHRA), or an integrated HRA, to supplement an existing employer-provided health insurance plan. Some employers that switch to higher-deductible group policies to offset rate hikes will offer a GCHRA to cover out-of-pocket costs such as annual deductibles, copays, and other healthcare expenses. However, group plan premiums are ineligible for reimbursement with a GCHRA.

With an HRA:

- The employer sets a defined monthly contribution amount, called an allowance, for each employee.

- While the QSEHRA has maximum annual limits, the ICHRA and GCHRA have no employer contribution limits.

- With a QSEHRA or ICHRA, employees purchase their preferred health insurance plan on a private or public exchange or the federal marketplace. For example, a young, single employee might opt for a high deductible plan (HDHP) to reduce their monthly premiums. In contrast, an older employee might choose a plan with a lower annual deductible and out-of-pocket maximum.

- If you have an integrated HRA, only employees enrolled in your employer-sponsored health coverage can participate in the benefit. They can’t have an individual plan only.

- Employees pay their monthly premiums and other medical costs out-of-pocket. Once they submit proper claim documentation, the employer reimburses them for eligible expenses up to their set allowance amount.

- Employees can’t exceed their allowance amount. Unlike health savings accounts (HSAs), any unused funds stay with you at the end of the plan year or if an employee leaves your company.

There are additional cost savings that come with an HRA. Reimbursements are tax-deductible and payroll tax-free for employers, which reduces your tax liability. They’re also free of income tax for the employee, as long as they purchase a medical plan that qualifies as minimum essential coverage (MEC).

Health insurance stipends

If you’re looking to add an HRA as your first health benefit or as a new option after cancelling your group health insurance policy, you’ll need to consider your employees’ eligibility for premium tax credits. Some of your employees might become eligible for premium tax credits without employer-sponsored health insurance coverage.

If your QSEHRA or ICHRA is affordable, employees can’t claim their premium tax credits. If your HRA benefit is unaffordable, employees can still access their tax credits. With an unaffordable QSEHRA, your employees must reduce their advance premium tax credit (APTC) by the amount of their QSEHRA allowance. Meanwhile, employees offered an unaffordable ICHRA have to choose between their tax credits and the ICHRA benefit.

Health stipends can help to alleviate these concerns. Stipends are essentially extra wages added to your employees’ paychecks that they can use to pay for their monthly premiums and other out-of-pocket costs. Stipends are flexible and have fewer regulations than HRAs, so they’re customizable enough for every organization.

If your employees receive tax credits, they can potentially keep those credits and take advantage of your health insurance stipend, depending on how the stipend impacts their income.

An important aspect to consider with health stipends is that they’re taxable. Unlike HRAs, you must report your stipend contributions on your employees’ W-2 at the end of each year.

Additionally, the federal government doesn’t consider stipends a formal health benefit, so applicable large employers (ALEs) can’t use them to satisfy the ACA’s employer mandate. Therefore, in many cases, an HRA is likely a better fit for your organization.

Conclusion

Employees today expect employers to offer health insurance, but many organizations find group health plans to be an expensive benefit. While there are a few ways to reduce employer health insurance costs, HRAs are affordable health benefits that give you more control over your medical expenses.

Employers prefer an HRA because it provides more budget flexibility, and employees can purchase a health insurance plan that meets their specific needs. If you think an HRA is right for your organization, schedule a call with a PeopleKeep HRA specialist to learn more.

This blog article was originally published on October 7, 2020. It was last updated on June 15, 2026.

References

1. KFF 2025 Employer Health Benefits Survey

2. pWc Report - Behind the numbers 2026

What percent of health insurance is paid by employers?

Wondering how much employers pay for health insurance? Learn the average employer contribution percentage and how it varies by plan and business size.

The least and most expensive states for individual health insurance

Discover the least and most expensive states for individual health insurance. Compare health insurance rates by state to plan smarter for coverage costs.

Health insurance reimbursements: What are the options?

Explore your options for health insurance reimbursement. Understand what insurance reimbursement means and how HRAs can support employees.