By Gabrielle Smith on August 10, 2021 at 8:05 AM

Since the individual coverage health reimbursement arrangement (ICHRA) was first available in 2020, employers both big and small have adopted the unique health benefit as a highly-anticipated alternative to traditional group health insurance.

With the freedom of no minimum or maximum contribution requirements, no business size restrictions, and flexibility with employee classes, it’s no overstatement to say that the ICHRA is poised to change the face of health benefits.

As the first company to deliver an ICHRA product to market, PeopleKeep is always at the forefront of new ICHRA developments. In this report, we’ll share unique customer data with year-over-year comparisons in allowance amounts, class sizes, expenses submitted and more, giving an inside perspective on how employers are using their ICHRA in 2021.

Download the visual report here

Allowances

To begin our analysis, we looked at how much of a monthly allowance employers are offering their employees. Overall, the average monthly allowance is $882.51, a 5% increase from last year’s average monthly allowance of $840.19. This is good news, as higher allowances offer an even more valuable health benefit for employees.

What’s more, comparing this monthly average to the cost of the lowest-cost self-only silver plan on the health insurance marketplace ($436), it’s clear to see that employees have enough to pay for their self-only coverage and still have funds left over toward family policies and other eligible medical expenses.

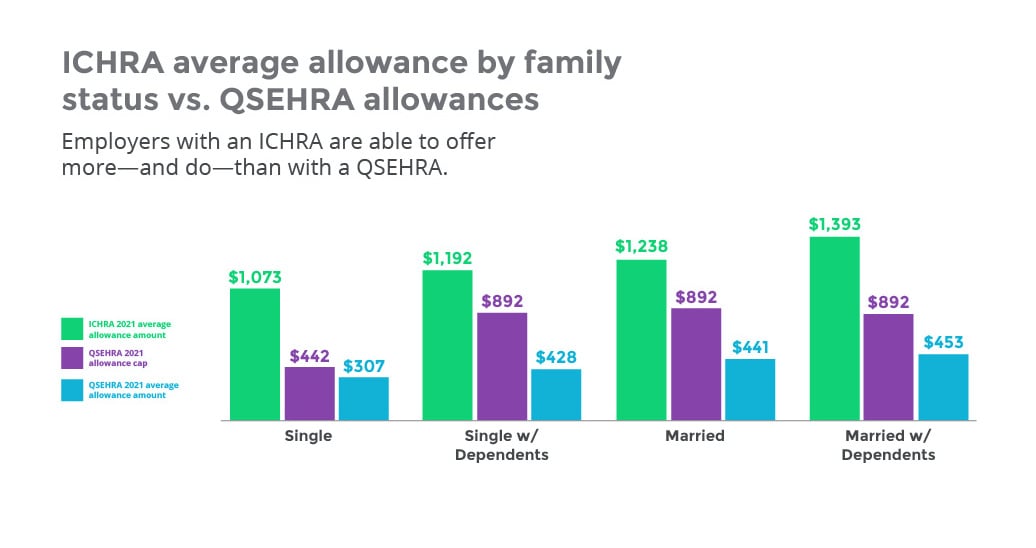

Average allowance by family status vs. QSEHRA allowances

Next, we drilled down the average allowance amount further to see if this figure changed when compared across family status, as well compared to what employers with a qualified small employer HRA (QSEHRA) are offering. After all, the QSEHRA comes with annual allowance caps that limit how much employers can offer, while the ICHRA has no such limitations.

The data show that employers are taking advantage of the lack of allowance restrictions, consistently offering higher allowance amounts than the 2021 QSEHRA allowance cap across all family statuses—in some cases as much as 142% more.

The monthly QSEHRA allowance cap in 2021 for single employees is $441.67 and $891.67 for single employees with dependents, married employees, and married employees with dependents. In that order, our report finds that the average monthly ICHRA allowance amounts for those statuses are $1,072.74, $1,192.43, $1,238.17, and $1,393.35.

Premium-only vs. premium-plus

The ICHRA allows for employers to choose between a premium-only or premium-plus account, depending on whether they want to reimburse their employees only for their health insurance premiums, or also reimburse them for qualifying out-of-pocket medical expenses.

When looking at how employers with a premium-only account use their benefit compared to employers with a premium-plus account, our analysis shows that, on average, the premium-plus accounts offer 93% more than employers with a premium-only account.

The overall national average for premium-only accounts is $800.08 and $1,545 for premium-plus accounts. This makes sense, given that employers with a premium-plus account intend their employees to purchase not only an individual insurance premium, but also a wide variety of over 200+ HRA-eligible healthcare expenses, including copays, prescription and nonprescription drugs, and even braces.

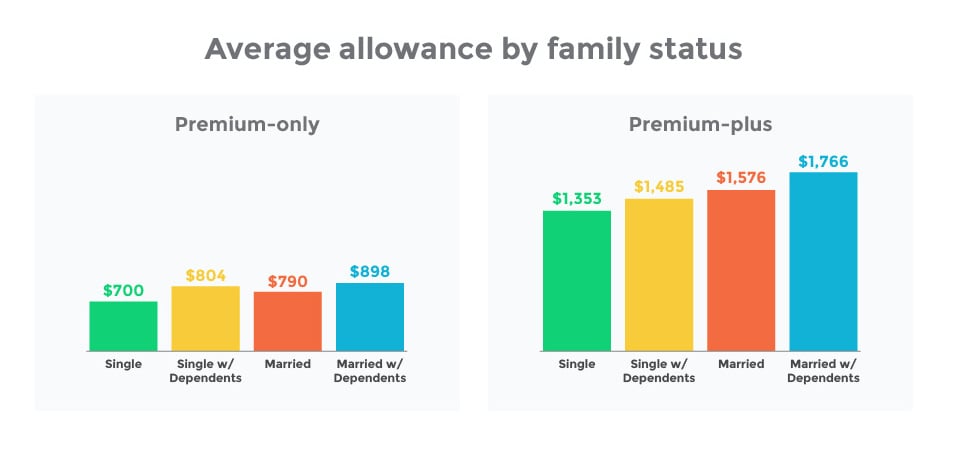

Average allowance by family status

When taking a closer look at the premium-only and premium-plus allowance amounts, the increased allowances for premium-plus accounts is consistent across family status.

For single employees, single employees with dependents, married employees, and married employees with dependents, the average allowance amounts for premium-only accounts are: $699.69, $789.67, $803.92, and $897.75. In the same order, the average allowance amounts for premium-plus accounts are: $1,352.95, $1,575.77, $1,484.88, $1,766.41.

Number of employers offering premium-only vs. premium-plus

Finally, in our analysis of premium-only and premium-plus accounts, we looked at how many employers are offering each type of account, and if applicable large employers (ALEs), who are eligible to offer an ICHRA under the Affordable Care Act, are more likely to offer a premium-only account than small and medium size businesses (SMBs).

Across all employers, regardless of size, 58% went with a premium-plus account, while the remaining 42% went with a premium-only account. ALEs opted for a premium-only account significantly more than the average.

With an ICHRA, employers can choose to offer their ICHRA benefit to certain classes of employees while offering a traditional group health plan to others—an option that’s not available with a QSEHRA.

However, among our ALEs, only 14% of them are utilizing this option. This tells us that offering a higher ICHRA allowance is generally seen as a more favorable option for ALEs than also investing time and money in administering a group health plan.

Classes

Another feature that’s unique to the ICHRA is the ability for employers to offer different allowance amounts to employees in different classes, such as by part-time, full-time, and seasonal workers, or even a combination of these.

Most popular classes

Among the eleven different classes available, the most popular option is to group all employees into one class and offer the same amount to all of them. Following that in popularity are full-time employees, full-time salaried employees, salaried employees, and part-time employees.

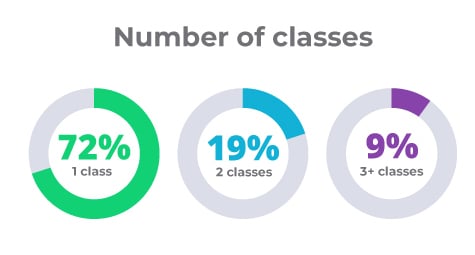

Number of classes

When looking at how many classes employers choose to divide their employees into, our analysis shows that most employers (72%) chose to only offer one class, while smaller percentages offered two (19%) and three or more (9%).

ALEs use classes differently than smaller employers

As we’ve already learned, ALEs use their ICHRA benefit differently than SMBs. This holds true when we look at the number of classes offered by ALEs compared to SMBs. The average number of classes for ALEs is 3.6, while for SMBs it’s only 1.4.

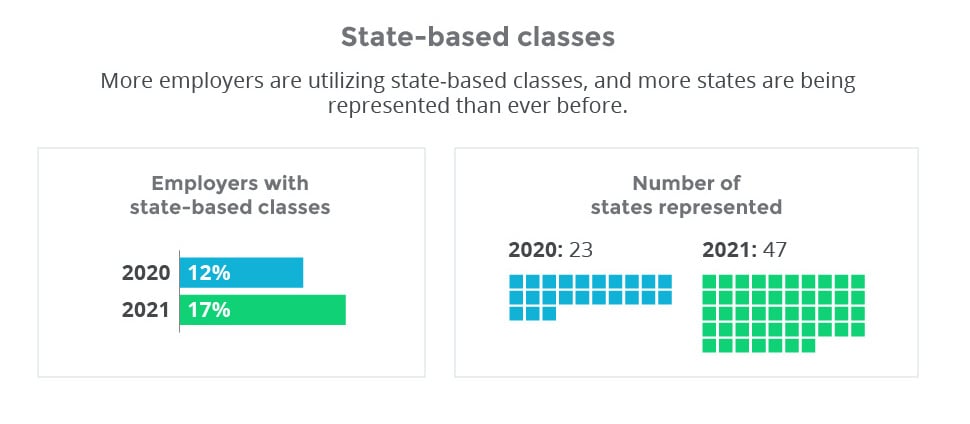

State-based classes

In a final look at ICHRA classes, we analyzed how many employers are dividing their employees using state-based classes. With more and more organizations going fully-remote, employees can be hired from all across the county, making the state-based class feature especially advantageous for today’s workforce. Compared to last year, 5% more employers utilized state-based classes and an additional 24 states were represented.

Out-of-pocket expenses submitted by employees

Lastly in our analysis, we looked into what out-of-pocket expenses employees are getting reimbursed through their ICHRA, and how much those expenses cost. Across both our QSEHRA and ICHRA customers, office visits and prescription drugs are consistently the most common out-of-pocket expenses submitted by employees.

On average, of employees who submitted expenses for reimbursement, 3.7 office visit expenses were submitted with an average reimbursement amount of $98.78. For prescription drugs, an average of 8.6 expenses were submitted with an average reimbursement amount of $95.72.

Knowing the average number and the cost of expenses submitted gives employers considering an ICHRA insight into how frequently employees are using the benefit and how much of a monthly allowance they should offer to meet their employees’ healthcare needs.

Conclusion

As demand continues to grow for a more affordable, flexible, and personalized health benefit, so too does the ICHRA’s popularity among employers of all sizes. Our report showcases that the ICHRA empowers employers to offer increased allowance amounts, include employees across multiple states, and reimburse their employees for not only a quality individual health insurance premium, but also a wide variety of out-of-pocket expenses.

If you’d like to learn more about the ICHRA and see how your organization can benefit from offering one, schedule a call with one of our benefits advisors today.

What is an ICHRA?

What is an ICHRA, and how does it work? Find out everything you need to know about this innovative healthcare option: the individual coverage HRA.

What we learned in the first 90 days of the individual coverage HRA

The long-anticipated individual coverage HRA (ICHRA) finally went into effect on January 1, 2020. Here is our 90-day report on how employers have used it.

Group health insurance vs. ICHRA

Trying to decide between group health insurance and an ICHRA? This guide breaks down the pros and cons of each to help you make an informed decision.